► ESOP (Employee Stock Ownership Plan). An ESOP is a form of defined contribution plan in which the investments are primarily in employer stock. A leveraged ESOP is an ESOP that finances its purchase of such stock through securities acquisition debt obtained from, or guaranteed by, the sponsoring employer. A leveraged ESOP, operated in accordance with applicable regulations, holds the shares purchased with the proceeds of such a loan in a “suspense account,” and releases them from the suspense account as the loan is repaid according to a set formula that is expressed in terms of number of shares.

ESOP Opportunity

- Owner wants a tax-free sale – C corporation

- Inside “confidential” transaction

- Use of other Qualified Plan assets tax-free

- Owner wants to stop paying taxes – S Corp.

- Deductibility of principle and interest – C or S

- Based on 1998 law: Sub-S Tax Exemption

- ESOP Promotion Act of 2004 – expands limit

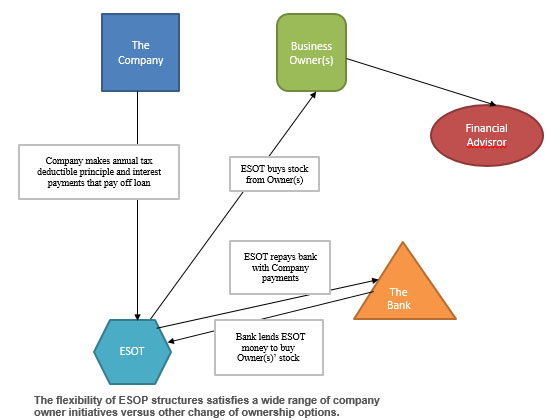

How it works:

- Set Up an ESOT

- ESOT Borrows from Bank

- ESOT buys stock from Owner

- Company makes annual contributions to ESOT

- ESOT receives contribution from Your Company

- ESOT repays Bank

- ESOT sets up account for each Employee

- Owner buys US securities from the Financial Advisor – non-taxable event (when C-Corp.)

Employee Stock Ownership Plans (“ESOPs”) provide:

- More opportunities related to transaction financing, and

- More control of the completion of the transaction.

- Tax deferred sale of company shares. Internal Revenue Code § 1042 provides beneficial tax treatment on shareholder gains when selling stock to an ESOP. Given certain conditions,

- Capital gains tax can be deferred allowing the full transaction proceeds to be invested in U.S. corporate stock and bonds [Qualified Replacement Property (“QRP”)].

- Long-term capital gains are recognized upon the liquidation of QRP securities at a future date after a required minimal holding period.

- If the QRP is not liquidated and becomes an asset of the seller’s estate, it has a stepped up basis and avoids capital gains completely.

- A corporation must have C status to receive the benefits of the 1042 rollover, which means that an S Corporation can change its status and receive the differed tax benefits without delay. However, this change in status can have negative tax effects that would cancel out any benefits gained from the 1042 rollover status due to different accounting methods, so a change in status may not always be the best option.

- § 1042 rollover requirements:

- The seller must have held the stock for at least 3 years;

- The ESOP must own at least 30% of the total stock immediately following the sale; and,

- The seller must reinvest the proceeds into QRP within a 12 month period after the ESOP transaction.

- QRP is defined as stocks and bonds of U. S. operating companies. (Not government securities.)

- The seller must invest in the QRP within a 15 month period (beginning 3 months prior to the sale and ending 12 months after the sale).

- The money that is invested can come from sources other than the sale, as long as that amount does not exceed the proceeds.

- Not all of the proceeds have to be reinvested. If the seller chooses to invest less than the sale price, then he or she will have to pay taxes on the amount not invested in QRP.

- In order to meet the 30% requirement, two or more sellers may combine their sales, provided that the sales are part of a single transaction.

- The sponsor company must be a C Corporation for selling the shareholder to qualify for a 1042 rollover.

- The shares sold to the ESOP cannot be allocated to the ESOP accounts of the seller, the relatives of the seller (except for linear decedents receiving 5% of the stock and who are not treated as more-than-25% shareholder by attribution), or any more-than-25% shareholders.

- Tax deductible Principal and Interest

Up to 25% of payroll may be deducted from Corporations Tax obligations where the employer makes principal payments on loans made to an ESOP trust in order to acquire employer securities on behalf of employees. Interest on ESOP loans is also fully deductible against Corporations Tax. (Where the ESOP is not financed by a loan, only up to 15% of payroll may be deducted.)

Usually, there is a 25% limit on tax-deductible contributions made by employers to ESOPs.

- C Corporations

- C Corporations do not have to count interest payments on ESOP loans as part of the 25% limit

- S Corporations

- The 1042 rollover option is not available to the shareholders.

- S Corporations have to count interest payments on ESOP loans as part of the 25% limit.

- Happy Employees. As owners, employees have a better attitude about increasing sales, reducing expenses, and overall being part of the business.

- Other

- ESOP Financing

- ESOP sellers can finance their own transactions.

- Banks look favorably on financing ESOPs.

- Employee Tax Deferral. Stock acquired for employees’ accounts is not taxed until distributed usually when the employee leaves the firm.

- Dividend Deductions. ESOP companies may claim a deduction for cash dividends paid on ESOP-held shares provided the dividends are either applied to repay an ESOP loan or paid out to employees.

- ESOP Financing

What to expect:

Details of the activities in each step are outlined below. While the list is abbreviated, it provides an overview of the ESOP Advisor team’s involvement in each step of the ESOP transaction.

- Independent Business Valuation

- Business Appraiser prepares an updated Business Valuation.

- Required standard of value is current Fair Market Value as defined in IRS Revenue Ruling 59-60 and subsequent rulings.

- Feasibility Study

- Interview & Data Request – Company management team is interviewed; financial and operational data is collected. ESOP Advisor performs due diligence and studies the issues affecting the company.

- Organizational Issues – Consider whether the management structure has the depth to continue operating as an autonomous, independent entity.

- Market Issues – Consider the company’s market viability, and review the company’s position in that market.

- Human Resource Issues – Evaluate management capability and continuity, in addition to the company’s ability to fill new and replacement positions.

- Operations – Assess the company’s supply chain, management control systems, productivity, and quality control.

- Financial Analyses – Analyze historical and prospective financial data, and determine if the payroll is adequate, in terms of IRC § 405 and § 415, to support a buyout.

- Business Valuation – Develop a letter summary fair market valuation of the proposed shares being sold to the ESOP.

- Legal Issues – Identify potential legal obstacles to an employee buyout, including pending litigation, environmental, pension, and corporate issues.

- Presentation – Written Feasibility Study is presented to company. Any negative findings are discussed, with plans made to address each.

- Arrange Financing

- Financing Memorandum – The Feasibility Study forms the basis of the Financing Memorandum for submission to ESOP funding sources.

- Lender Submission – Financing Memorandum and Proposal is prepared, and application is made to select affiliated ESOP lenders.

- Negotiate Financing Terms – Buyout loan terms, including representations and warranties, are negotiated with lender on company’s behalf.

- Plan & Trust Development

- Establish ESOP Committee – The ESOP Committee may be composed of company management and staff personnel, although initially it includes only the seller(s).

- Plan & Trust Design – Plan and Trust Document drafts are prepared by ESOP Affiliates to minimize legal input and corresponding fees. Summary Plan Description (SPD) is prepared and reviewed.

- Engage Law Firm – Engage and manage affiliated law firm with specific ESOP experience.

- Establish Trust – Establish employee stock ownership trust to acquire majority shareholder’s stock. Trustee can be current company owner, management personnel, or third-party trust firm.

- Plan Document – Review SPD and prepared Plan Document, making any changes to conform to current tax and labor law. Prepare stock sale agreement and other transaction documents.

- Determination Letter and Bank Documents – Send request for determination letter to the Internal Revenue Service. Review and negotiate loan documents with bank

- Close

- Communicate Plan to Employees – Introduce conceptual framework to employees, and establish a strong communication channel to ensure comfort level.

- Close Transaction – The transaction is closed, with sales proceeds being disbursed accordingly. All transaction and loan documents are executed.

- Complete Plan Structure – Assign positions within the ESOP Committee, develop communication vehicles and frequencies.

- Hire Plan Administrator – Plan Administrator must be a specialist in ESOP administration.

- Education – Continue employee education process to ensure full understanding of ESOP benefits and the resulting increase in employee motivation.

- Repurchase Planning – Developing repurchase liability plan through insurance or investment products.

How it Works:

ESOP (Employee Stock Ownership Plan) – An ESOP is a form of defined contribution plan in which the investments are primarily in employer stock. A leveraged ESOP is an ESOP that finances its purchase of such stock through securities acquisition debt obtained from, or guaranteed by, the sponsoring employer. A leveraged ESOP, operated in accordance with applicable regulations, holds the shares purchased with the proceeds of such a loan in a “suspense account,” and releases them from the suspense account as the loan is repaid according to a set formula that is expressed in terms of number of shares.

ESOP Opportunity

- Owner wants a tax-free sale – C corporation

- Inside “confidential” transaction

- Use of other Qualified Plan assets tax-free

- Owner wants to stop paying taxes – S Corporation

- Deductibility of principle and interest – C or S

- Based on 1998 law: Sub-S Tax Exemption

- ESOP Promotion Act of 2004 – expands limit

Architecture of an ESOP

| Minimum Size of Company |

Small | Large | Small | Small | Small | Small |

| Ability to Sell Shares Now |

Yes | No | Yes | No | Yes | Yes |

| Partial Sale Option |

No | Yes | Yes | No | Yes | Yes |

| Probably of Success |

Medium | Low | High | High | High | High |

| Remain Independent |

No | Yes | Yes | Yes | Yes | Yes |

| Tax Deferred Proceeds |

No (unless merger) |

No | No | No | Yes | Yes – C Corp; No – S Corp; (Yes with seller note) |

| Tax Deductible Contributions |

NA | NA | No | No | Yes | Yes |

| Maintain Control |

No | Public Scrutiny |

No | Yes | Yes | Yes |

| Employee Security |

Low | High | High | High | High | High |

| Promote Productivity |

No | No | No | Yes | Yes | Yes |

| Key Employee Incentive |

Depends on Buyer |

Usually | No | Yes | Yes | Yes |

| Typical Time to Completion |

6 – 12 Months |

6 – 12 Months |

2 Weeks | 2 Weeks | 2 – 6 Weeks |

2 – 6 Weeks |

| Fees | Large | Large | Small | Small | Small | Small |

The following information is provided with permission of the National Center for Employee Ownership, a nonprofit membership and information organization.

Are ESOPs Really More Complex Than Other Ways to Sell a Business?

Using an ESOP for Business Transition Can Be Complicated, But Selling to an Outside Buyer Is Often Uncertain and Even More Complicated

When people describe the pros and cons of ESOPs, often they note that the plans are complex. ESOPs are somewhat more complex than 401(k) and similar retirement plans and do cost substantially more to install and somewhat more to operate, mostly because an annual appraisal is required for closely held companies. But ESOPs are not more complex than selling to a third party.

The table below compares what issues come up in the sale of a company to an ESOP compared to a sale to a third party. It was prepared with the advice of professionals who have done both kinds of transactions.

The table indicates that the overall level of complexity is similar, but ESOPs are much less risky in terms of the likelihood of finding a buyer. They are also considerably less costly, mostly because in the case of a sale to a third party, in addition to substantial legal, accounting, and sometimes other fees, the price paid to the seller is usually reduced by brokerage commissions paid by the buyer.

| ESOP | Sale to Another Company | |

|---|---|---|

| Key legal documents |

|

|

| Feasibility studies and preparation |

Feasibility studies assess whether the company has sufficient payroll and cash flow to buy the desired amount of stock. Can be performed internally or with expert advice. Forensic due diligence rarely needed. | Companies must prepare a detailed and accurate description of the firm and its finances, prospects, and risks. Buyers will want to do a forensic due diligence investigation and sellers should do the same to assess the financial soundness of the buyer and the terms of the offer. |

| Valuation | Outside appraisal required; valuation based on fair market value | In smaller deals, outside appraisal not required but recommended; in larger deals price usually set by controlled auction. |

| Terms and risks |

Plans can be structured in a variety of ways:

|

Buyers will typically have multiple contingencies:

|

| Time to sell | Once the seller has decided on doing an ESOP and its basic structure, four to six months. | Median formal offer to sale time is 10 months for companies in the small to mid-market range. |

| Role of seller post- transaction |

Flexible depending on seller interests | Buyer will usually determine role in smaller deals; in large deals role is usually negotiable. |

| Sale of minority interest |

ESOPs can buy any percentage of stock from any number of sellers | Buyers almost invariably want to buy the entire company |

| Success Rates | If an ESOP is determined to be feasible, only rarely do transactions fall through once a decision to proceed has been made | Overall, only about 25% of privately held businesses put up for sale are sold and only about 50% of businesses with 100 or more employees are sold. |

| Transaction costs |

|

|

Ownership Transitions: ESOPs Compared to Other Strategies

by Kelly Finnell, Executive Financial Services

There are three traditional ownership succession strategies: sell to an insider, sell to an outsider and “till death do us part.” Each of these traditional options are compared an ESOP.

1. Sell to an Insider

“Insiders” refer to a company’s current employees and to the current owner’s family members. In many closely held companies, family members (sons, daughters, brothers, sisters, etc.) and/or employees who are most important to the company’s success are the insiders who will take over the business when the owner leaves.

Insiders almost never have the cash and/or credit that is needed to purchase the company. Therefore, if they are to purchase the company, the acquisition must be “boot strapped.” This is where the company bonuses them the cash that is needed for the purchase. Unfortunately, the tax-bite involved in this process makes it very financially inefficient

The following chart assumes that an insider wants to purchase stock valued at $10,000,000 from a current owner. The insider will either borrow $10,000,000 from a bank with the company as a guarantor; or the current owner will sell to the insider for a $10,000,000 promissory note guaranteed by the company. In either case, the company will bonus the insider the cash he or she needs each year to service the debt. The following chart illustrates the company cash flow that is required in order for the insider to have $10,000,000 net after-tax to pay the selling shareholder.

| Total Bonuses Paid: | $16,556,291 |

| Taxes on Bonuses: | $6,556,2915 |

| Net Remaining: | $10,000,000 |

As you can see from this chart, because the insider needs $10,000,000 to service the debt and since the bonuses he receives are taxable to him, the company must bonus him $16,556,291 in order for him to have the $10,000,000 net. Therefore, this structure requires 66% more company cash flow due to the tax bite.

Here is the math used in this chart: $10,000,000 ÷ .65 = $16,556,291. $10,000,000 is the amount needed to service the acquisition loan. .604 is 100 minus the insiders’ tax rate (.396).

Using an ESOP as the purchaser “on behalf of” the Insider, saves $6,556,291. This is the result of two things:

- the company receiving a tax deduction for the ESOP contribution used to service the acquisition debt,

- the insider not having to pay tax on the $10,000,000 the company contributes to the ESOP. This 66% cost savings makes an ESOP a much more financially efficient strategy than a traditional sale to an insider.

2. Sell to an Outsider

“Outsider” refers to several types of potential buyers, including: competitors, private equity groups (PEGs), suppliers, individual investors, etc. There are many advantages to selling to an outsider but these advantages are not as attractive as they may first appear. In fact, according to one source, 75% of people who sold their company to an outsider later regretted their decision. Below are the major benefits of selling to an outsider with some of the caveats you should consider.

Cash Out and Move On

Many business owners assume that when they sell their company they will receive cash at closing and will be able to retire the next day. That is almost never the case. Buyers want to make sure that the company they are purchasing will continue to grow and prosper after closing. In order to protect themselves from a negative surprise, purchasers often structure sales agreements containing some or all of the following provisions: earn-outs, escrows/holdbacks, consulting/employment agreements, and covenants not to compete.

Earn-outs are designed to protect a purchaser from overpaying for the company it is buying. Purchasers are almost always buying a company’s future cash flow. If a purchaser expects a company’s future cash flow to be $2,000,000 per year, the purchaser might agree to pay $10,000,000 for the company. If the company’s cash flow drops to $1,000,000 per year immediately after the sale is consummated, the purchaser will have paid two times the cash flow multiple it anticipated ($10,000,000 purchase price/$1,000,000 cash flow results in a valuation multiple of 10x instead of the 5x multiple the purchaser intended to pay).

Here is how a purchaser could have protected himself from overpaying in the above example. Instead of agreeing to pay 5-times cash flow at closing, the purchase agreement could have included an earn-out provision. A purchase agreement with an earn-out might be structured as follows:

Step 1:

The purchaser agrees to pay 2.5 times the 3 previous years’ average annual cash flow at closing. Assuming annual cash flow of $2,000,000 over the previous 3 years, the purchaser will pay $5,000,000 at closing. The purchase agreement in this example may state that the purchaser will make payments on the first two anniversaries of the closing of the sale (“earn-out payments”). The purchase agreement may state that on each anniversary if the previous year’s cash flow is $1,000,000-$2,000,000 the earn-out payment will equal 2.5 times the amount in excess of $1,000,000.

Step 2: The earn-out formula would then be:

(Cash flow – $1,000,000) x 2.5

The purchase agreement may further state that if cash flows exceed $2,000,000, the earn-out payment will be calculated as follows

$2,500,000 + (Cash flow – $2,000,000)x 1.5

The $2,500,000 would be the earn-out payment on the first $2,000,000 of cash flow. This second payment at (1.5x) would generally be referred to as a “bonus” earn-out payment.

If cash flow is less than $1,000,000, no earn-out payments would be made. Several examples are shown below.

If the company continues to have $2,000,000 of cash flow following the sale, the sellers would receive the following payments:

Closing Payment (2.5 x $2,000,000)= $5,000,000

1st Anniversary ($2,000,000 – $1,000,000) x 2.5 = $2,500,000

2nd Anniversary ($2,000,000 – $1,000,000) x 2.5 = $2,500,000

Total Purchase Price = $10,000,000

Purchase Price/Average Annual Cash Flow = 5

If the company has cash flow of $1,500,000 the first year following the closing of the sale and $1,200,000 the second year following closing, the sellers would receive the following payments:

Closing Payment (2.5 x $2,000,000) = $5,000,000

1st Anniversary ($1,500,000 – $1,000,000) x 2.5 = $1,250,000

2nd Anniversary ($1,200,000 – $1,000,000) x 2.5 = $500,000

Total Purchase Price = $6,750,000

Purchase Price/Average Annual Cash Flow = 5

In this case the purchaser would have successfully protected itself using an earn-out provision. Cash flow over the 2-years following the sale averaged $1,350,000. The purchaser paid $6,750,000 for the company resulting in it paying a multiple of 5-times post-sale average annual cash flow ($6,750,000 ÷ $1,350,000 = 5).

If the company’s cash flow decreased to $1,000,000 or less after the sale, the purchaser would not make any payments following the closing payment of $5,000,000.

If the company’s cash flow increased to $3,000,000 per year for the 2-years following closing, the seller would receive the following payments:

Closing Payment (2.5 x $2,000,000) = $5,000,000

1st Anniversary ($2,500,000 + ($3,000,000 – $2,000,000)x 1.5) = $4,000,000

2nd Anniversary (same as 1st above) = $4,000,000

Total Purchase Price = $13,000,000

Purchase Price/Average Annual Cash Flow = 4.33

In this case the purchaser paid $3,000,000 more than it would have paid without the earn-out but its purchase price multiple would be less than the 5x it was willing to pay for the company’s future cash flow. The sellers also would have benefited by receiving the additional $3,000,000. This earn-out formula with a bonus payment for “excess cash flow” was a good deal for both parties.

There are many ways to structure earn-outs and this is just one example. The point is not that your earn-out will be structured as illustrated above. Rather the point is that purchasers are very careful not to overpay for a company and, as a result, your sales agreement is likely to contain an earn-out, particularly when a purchase price cannot be agreed upon. Therefore, when you sell to an outsider, you probably will not be able to cash-out and move on immediately following the sale.

Sales agreements almost always include “representation and warranties” in which the seller states certain facts about the condition of the business. If these facts later turn out not to be accurate, the purchaser may have a financial claim against the seller. To streamline collecting on this financial claim and avoid having to bring suit against the seller for the amount claimed, a portion of the sales proceeds may be placed in escrow at closing. A typical escrow amount is 10%. A typical escrow period is 2 years.

Here is how an escrow might impact the timing of payments in the scenario described above.

- The seller would receive $1,500,000 at closing instead of $2,500,000;

- $1,000,000 would be placed in escrow by the purchaser;

- The seller would be paid the $1,000,000 escrow amount in 2 years when the escrow period expires (if the purchaser does not make a claim against the escrow).

Escrows present an additional hurdle to sellers being able to cash out and move on immediately following a sale.

Sales agreements generally include provisions preventing the seller from competing against the purchaser or “pirating” the company’s customers. In addition, sales agreements often contain provisions requiring the seller to work for the company for 1-3 years following the sale. This prevents the seller from retiring immediately after the sale is closed.

Sometimes people say that they do not want to do an ESOP because it will not allow them to exit their company immediately following the sale. While this is true, the same can be said about a sale to an outsider. Owners of closely held companies are almost never able to sell their company and walk away regardless of whether they sell to an Insider, an Outsider or an ESOP.

Taxes

Most business owners know that if they sell stock that they’ve owned for at least one year, they will pay tax at long-term capital gain tax rates rather than at ordinary income tax rates. Currently, the federal long term capital gains tax rate is 20% (plus a 3.8% Medicare surtax) and the maximum ordinary income tax rate is 39.6%. Therefore, being able to pay tax at the capital gains tax rate results in a savings of 39.8%.

Many business owners assume that when they sell their company they will pay long-term capital gains tax on the sales proceeds and will enjoy the tax savings described above. However, this often is not the case.

The taxation of proceeds from the sale of a company will depend on several factors. The principal factors are:

- whether the sale is structured as a stock sale or an asset sale; and

- whether the company is a C corporation or a “pass through” entity such as an S corporation or LLC (Limited Liability Company).

If the sale is structured as a sale of stock, the tax consequences will be the same regardless of whether the company is a C corporation or an S corporation: The sellers will pay long-term capital gains tax on the amount of sales proceeds they receive in excess of their tax basis. Obviously, this is the best possible result for the sellers. However, purchasers almost always prefer purchasing a company’s assets rather than its stock.

The first reason acquirers prefer purchasing assets, is because when doing so they only assume liabilities directly associated with those assets – such as mortgages. If an acquirer purchases a company’s stock, the acquirer assumes all of the company’s liabilities – known and unknown. This includes errors and omissions, product liability, environmental, etc. In a small transaction (less than $100,000,000) the cost of due diligence to assure that there are no such liabilities is not justified by the size of the deal. Therefore, most potential acquirers will insist on purchasing assets.

The second reason acquirers prefer purchasing assets is that doing so increases the acquirer’s tax benefits. This tax advantage is best illustrated by an example.

- Assume that an acquirer pays seller $10,000,000 for company stock. The assets of the purchased company will retain the same tax basis they had prior to the acquisition.

- Assume that the total tax basis of all the assets was $3,000,000. The acquirer has paid $10,000,000, but has a tax basis in the company’s assets for depreciation purposes of $3,000,000.

- If the purchaser had purchased the company’s assets, the tax basis of those assets would have been “stepped-up;” i.e., increased to the amount paid for each asset. This could increase the acquirer’s future tax benefits on the depreciation of these assets dramatically. (Please note that a stock sale coupled with a Section 338 election may achieve virtually the same result, depending on the circumstances).

If the sale is structured as an asset sale, the tax consequences to the seller will depend upon whether the company is a C corporation or a pass through entity.

If it is a C corporation, the tax consequences of an asset sale can be confiscatory. In an asset purchase, the sales agreement is between the purchaser and the company – not the purchaser and the shareholders. If the purchaser pays $10,000,000 for the company’s assets, the payment is made to the company, not the shareholders.

C corporations (unlike their shareholders) pay tax on the sale of assets at ordinary income tax rates (potentially 35%) rather than capital gains rates (20, plus a Medicare surtax of 3.8%). After a C corporation has received the sales proceeds and paid the tax associated with the sale, it then distributes the net amount to its shareholders who pay the 20% (plus a Medicare surtax of 3.8%) rate on “qualified dividends.” This results in a double layer of tax. The chart below shows the total tax liability on a C corporation asset sale followed by a shareholder distribution.

- Asset Sales Proceeds: $ 10,000,000

- Assets’ Tax Basis: $ 3,000,000

- Taxable Gain: $ 7,000,000

- C Corporation Tax (34%): $ 2,380,000

- Net Distribution to Shareholders: $ 7,620,000

- Shareholder Tax (20% + 3.8%): $ 1,813,560

- Net Sales Proceeds: $ 5,806,440

Now you understand what was meant earlier that a C corporation asset sale can result in a confiscatory rate of tax – in this example over 42% of the sales proceeds and approximately 60% of the taxable gain will be paid in taxes.

If the company is a pass-through entity (S corporation, partnership, or LLC), an asset sale results in far less tax. This is due to the fact that since pass-through entities do not pay federal tax, there is only one, rather than two, levels of taxation. Whether the tax will be at ordinary income tax rates or at capital gains tax rates will depend upon the asset being sold.

Returning to our earlier example of a $10,000,000 company, let’s “drill down” and look at the assets it owns.

| Basis | FMV | Gain | Tax | |

| Accounts Receivable | $0 | $1,000,000 | $1,000,000(1) | $396,000 |

| Inventory | $1,000,000 | $2,000,000 | $1,000,000(1) | $396,000 |

| Warehouse | $1,500,000 | $4,500,000 | $3,000,000(2) | $714,000 |

| Land | $500,000 | $500,000 | $0 | $0 |

| Goodwill | $0 | $2,000,000 | $2,000,000(1) | $792,000 |

| Total | $3,000,000 | $10,000,000 | $7,000,000 | $2,298,000 |

| (1)indicates an asset whose gain is taxed as ordinary income (2)indicates an asset whose gain is taxed as a capital gain. |

The effective tax rate on the sales proceeds is 22.98% ($2,298,000 tax liability divided by the $10,000,000 sales proceeds). The effective tax rate on the “taxable gain” is 32.8% ($2,298,000 tax liability divided by the $7,000,000 taxable gain).

If you receive an offer from an outsider to purchase your company, you should ask your accountant to calculate the taxes that will be due on your sales proceeds and the after-tax amount you will be able to “bank” after the sale. You might want to compare the net after-tax proceeds you will receive from a sale to an outsider versus the amount you will receive from a sale to an ESOP.

When an owner sells to an ESOP, he or she almost always sells stock (more than 99% of the time). If the company is an S corporation at the time of the sale, the owner will pay tax at capital gains tax rates. If the company is a C corporation, the owner may be able to defer tax, perhaps even permanently. In either event, a sale to an ESOP will, in most situations, result in substantial tax savings for the selling shareholders.

Maximize Price

Many of the business owners assume that they will be paid more if they sell to an outsider than if they sell to an ESOP. In most cases, this is not true.

In general, there are two types of buyers: financial buyers and strategic buyers.

A financial buyer purchases a company for its future cash flow and pays the seller a multiple of cash flow based upon prevailing market conditions. For example, a financial buyer, such as a private equity group (PEG) or a private investor may pay five times the company’s expected future cash flow, generally defined as Earnings Before Interest Taxes Depreciation and Amortization (EBITDA). An ESOP is not allowed to pay more than the maximum amount a financial buyer would pay but an ESOP can pay as much as any other financial buyer.

A strategic buyer, such as a competitor or supplier, may pay more than a financial buyer because of potential cost savings, new revenue opportunities and other synergies. Business owners may receive a higher price from a strategic buyer than they could receive from an ESOP or other financial buyer.

Therefore, it is not entirely true that an ESOP cannot pay as much as other buyers. An ESOP can pay as much as other financial buyers, which may be less than what a strategic buyer would pay.

3. Till Death Do Us Part

Some business owners say they want to “die with their boots on.” Often these individuals are passionate about their work, or have their work and much of their identity and self-worth tied to their involvement with their company. It’s not unusual to see these business owners work well into their 70’s and 80’s

There are several risks inherent in a “till death do we part” strategy.

During the economic turmoil that engulfed the world beginning in the later part of 2007, many business owners who had been highly successful for decades saw their companies suffer a dramatic downturn or even fail. Companies involved in manufacturing and construction were particularly hard hit.

Consider a 70-year-old business owner who in July 2007 had a construction or manufacturing company worth $10,000,000, 401(k) and personal investments worth $2,000,000, and a home and personal property worth $1,000,000. Eighteen months later his home and 401k could have dropped in value 20%-40%, and his construction or manufacturing company could have been liquidated, with the proceeds used to pay off its debts.

Most of us know someone who experienced this type of financial meltdown. The lesson to be learned is that diversification and asset allocation are critical to protecting our financial security. What would have happened to this business owner if he had sold 50 percent of his company to an ESOP for $5,000,000 prior to the economic downturn and invested that money very conservatively? He would have lost some of his net worth as a result of the recession, but he would have been much more financially secure. Selling to an ESOP would have enabled him to have enhanced his financial security while allowing him to continue to work for and to control his company for as long as he chose to do so.

Another risk inherent in a “till death do us part” strategy is the risk of disability or pre-mature death. In many small to midsize companies if the owner becomes disabled or dies, the company may have to be sold for a fraction of its value. Owners can protect themselves from this risk with buy-sell agreements and with disability and life insurance, but ESOPs also can play a valuable role.

The final risk inherent in a “till death do us part” strategy is the potential loss of key employees. Here’s a common situation: A company with a single owner who is age 55 has a 30 year old key employee who the owner thinks will be able to run the company after he is gone. Here’s the dilemma: if the owner plans to work his entire life, how can he keep the key employee “engaged” for the next 20 years?

As you undoubtedly know, we entrepreneurs are inpatient by nature. Therefore, a young key employee who truly will be able to run your company some day likely will not be satisfied with you telling him that he can purchase your company from your estate after you die. Any successor who is worth having is going to be too impatient to accept this type of amorphous planning. Instead, the successor is going to want to see a more concrete planning structure in place and he is going to want to have some significant role and decision making authority before the time he is 55 (in our example, the key employee is 30 and the owner’s life expectancy is 25 years).

Conclusion

When it comes to succession planning, there is no single strategy that works best in every situation. The goal in elaborating on some of the problems inherent in the three traditional strategies (Sell to an Insider, Sell to an Outsider, and “Till Death Do Us Part”) is not to discourage you from employing one of them. Rather, to provide an honest and balanced comparison of the advantages and disadvantages of these traditional strategies compared to an ESOP. This should help you select the strategy that works best for you.